How Women Can Navigate the Path to Ownership with Confidence

In recent years, single women have emerged as a powerful force in the real estate market, breaking barriers and taking control of their financial futures. According to recent data, single women now own more homes than single men, with nearly 20 million women homeowners in the U.S., representing a growing trend of resilience and empowerment. This surge in homeownership among women has come even in the face of economic challenges, including the financial fallout of the pandemic.

In recent years, single women have emerged as a powerful force in the real estate market, breaking barriers and taking control of their financial futures. According to recent data, single women now own more homes than single men, with nearly 20 million women homeowners in the U.S., representing a growing trend of resilience and empowerment. This surge in homeownership among women has come even in the face of economic challenges, including the financial fallout of the pandemic.

Whether you’re already envisioning your dream home or just starting your search, navigating the homeownership journey as a single woman comes with unique considerations.

1. Assess Your Financial Health

The first step toward homeownership is a thorough assessment of your financial situation. Start by reviewing your credit score, savings for a down payment, and monthly budget. This will give you a clear picture of what you can comfortably afford. Understanding your finances also empowers you to make realistic homeownership goals that align with your current and future needs.

2. Explore Your Financing Options

The mortgage market can feel overwhelming, especially if you’re a first-time homebuyer. Fortunately, there are several programs available that can help make homeownership more accessible. These include:

- FHA Loans: Known for lower down payment requirements and more flexible credit standards, making them ideal for solo buyers.

- Conventional Loans: Best for those with strong credit and a larger down payment.

- Down Payment Assistance Programs: Many states and local governments offer grants or loans that can help reduce your upfront costs.

- First-Time Homebuyer Programs: These programs provide reduced interest rates, lower fees, or other forms of financial assistance for those purchasing their first home.

By exploring these options, you can find the program that best fits your financial situation, making the homeownership dream a reality.

3. Define Your Homebuying Vision

Homeownership is a personal decision, and your priorities might look different from those of other buyers. As a single woman, you’re in a unique position to design your homebuying journey around your specific needs, lifestyle, and goals.

Do you want a peaceful retreat in the suburbs, where you can unwind after a busy day? Or does the convenience and excitement of urban living, with proximity to work and social activities, better align with your goals?

By clearly defining your “must-haves” early in the process, you can focus your search on homes that reflect your vision for the future, making it easier to narrow down options and stay on track.

4. Build Your Support Network

Navigating the homebuying process on your own can feel overwhelming, but you don’t have to do it alone. Surround yourself with a reliable team of professionals who can guide and support you throughout your journey:

- A real estate agent who understands your goals and the local market.

- A loan officer who can help you evaluate financing options and walk you through the mortgage process.

- Friends and family who can offer emotional support, share advice, and encourage you along the way.

This team of professionals, combined with the support of your loved ones, will provide the expertise and encouragement you need to make confident decisions throughout the home-buying process.

5. Stay Patient and Stay Informed

The real estate market is constantly evolving, with interest rates, inventory levels, and home prices fluctuating regularly. Staying informed about current market trends will help you make well-timed decisions and avoid the temptation to rush into a purchase.

Patience is key. Don’t feel pressured to settle for a property that doesn’t meet your needs, financial goals, or vision for the future. Trust that the right opportunity will come along if you remain proactive and informed.

Empowerment Through Homeownership

The rise of single women homeowners is a powerful reminder of the increasing financial independence and strength of women across the country. Homeownership represents more than just owning property; it’s about securing a stable future, building equity, and creating a space that truly reflects your unique lifestyle and aspirations.

With careful planning, the right support, and a clear vision, more women are leaping into homeownership, setting themselves up for long-term success. If you’re ready to begin your journey, know that the tools and resources are available to help you achieve your dream of homeownership.

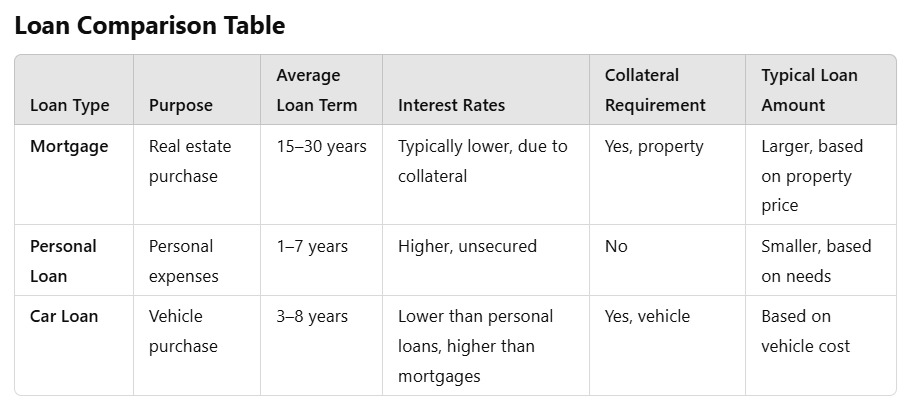

Planning to buy a home, finance a car, or cover unexpected expenses? Many loan options exist to help you achieve your financial goals, but choosing the right one can be challenging. Here’s a breakdown of the most popular types of loans, their unique characteristics, and what you need to know to make the best choice for your financial future.

Planning to buy a home, finance a car, or cover unexpected expenses? Many loan options exist to help you achieve your financial goals, but choosing the right one can be challenging. Here’s a breakdown of the most popular types of loans, their unique characteristics, and what you need to know to make the best choice for your financial future.

Buying a home is a huge milestone, and the excitement of closing can lead many buyers to quickly accept any mortgage offer without fully understanding its terms. One important detail to watch for is whether your mortgage includes a prepayment penalty. This fee can be an unwelcome surprise, so it’s crucial to know what you’re signing up for before finalizing your loan.

Buying a home is a huge milestone, and the excitement of closing can lead many buyers to quickly accept any mortgage offer without fully understanding its terms. One important detail to watch for is whether your mortgage includes a prepayment penalty. This fee can be an unwelcome surprise, so it’s crucial to know what you’re signing up for before finalizing your loan. When it comes to protecting one of your most significant investments—your home—having the right insurance coverage is essential. Home insurance, also known as homeowners’ insurance, offers financial protection against a wide range of potential risks, from natural disasters to theft. However, not all home insurance policies are created equal. Understanding the different types of home insurance coverage can help you make an informed decision that best suits your needs. We will touch on the various types of home insurance coverage available and what each one entails.

When it comes to protecting one of your most significant investments—your home—having the right insurance coverage is essential. Home insurance, also known as homeowners’ insurance, offers financial protection against a wide range of potential risks, from natural disasters to theft. However, not all home insurance policies are created equal. Understanding the different types of home insurance coverage can help you make an informed decision that best suits your needs. We will touch on the various types of home insurance coverage available and what each one entails. Buying a home is a significant investment, and ensuring the property is in good condition is crucial. There are times when asking the seller for repairs is the best course of action, but in other situations, requesting a credit may be more beneficial. Understanding when to choose each option can help you navigate the buying process more effectively.

Buying a home is a significant investment, and ensuring the property is in good condition is crucial. There are times when asking the seller for repairs is the best course of action, but in other situations, requesting a credit may be more beneficial. Understanding when to choose each option can help you navigate the buying process more effectively.